Why Crypto Markets Will Ultimately Converge on Full-Chain Trading Platforms

From Bitcoin to stablecoins, and from CEX-vs-DEX to the next generation of trading infrastructure.

- Crypto is moving from asset issuance to infrastructure competition: the scarce resource is no longer tokens, but trading systems.

- CEXs solve usability but concentrate trust; traditional DEXs preserve on-chain verifiability but still struggle to behave like complete trading systems.

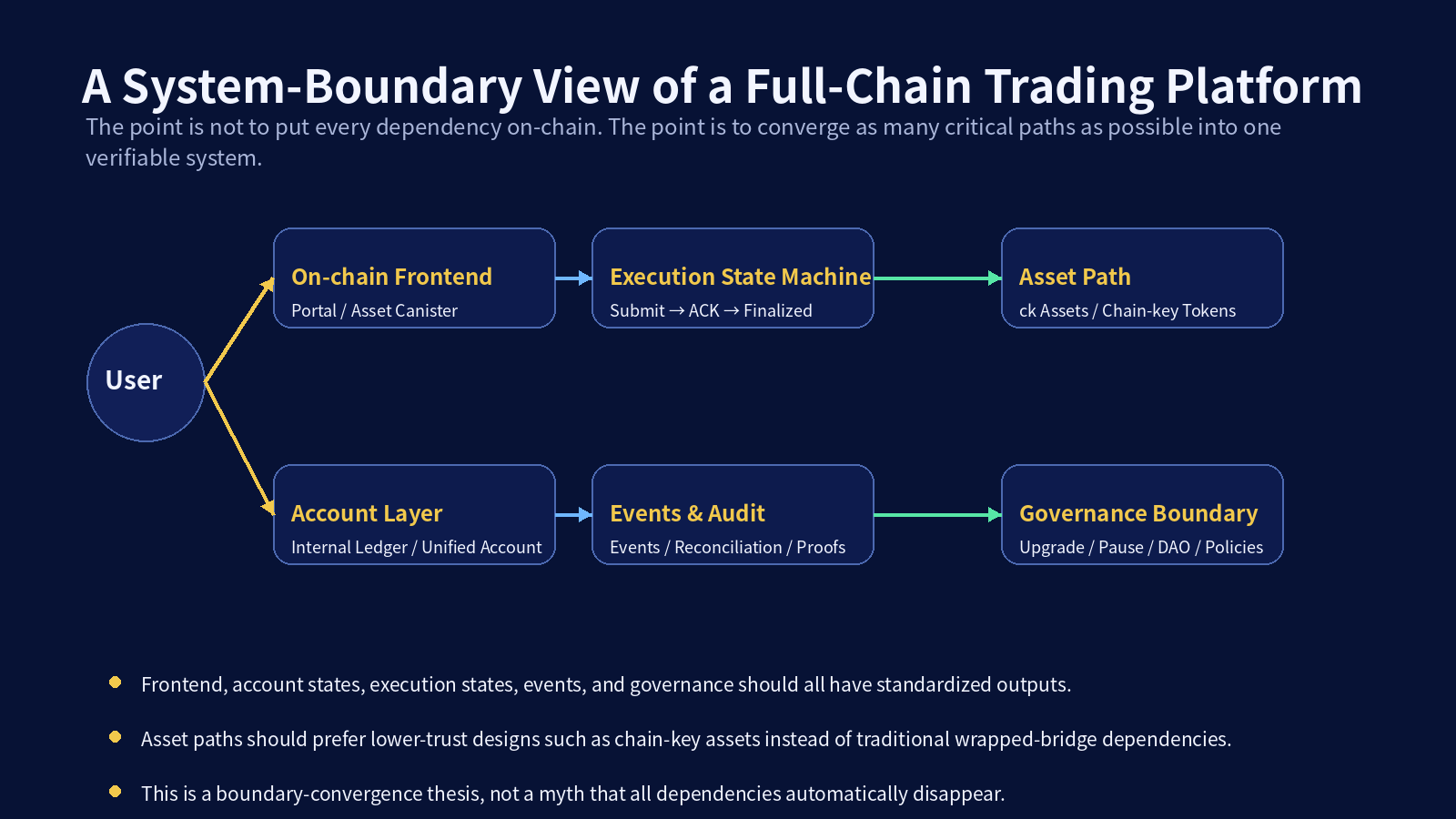

- A full-chain trading platform does not simply put everything on-chain; it converges the critical paths of trading toward one verifiable system.

- SSS is an attempt to build that system on ICP through acceptance determinism, a unified internal ledger, auditability, and a tighter end-to-end trust boundary.

Why Crypto Markets Will Ultimately Converge on Full-Chain Trading Platforms

From Bitcoin to stablecoins, and from CEX-vs-DEX to the next generation of trading infrastructure

Crypto has entered a new phase. The core debate is no longer just whether on-chain assets matter. The more important question now is this: as assets, settlement, and capital flows move on-chain, what form will the trading system itself take?

Bitcoin introduced peer-to-peer value transfer without relying on a financial intermediary. Ethereum expanded that model into an open platform for programmable assets and applications. Stablecoins then pushed the on-chain world from a largely speculative environment toward a real settlement and dollar-liquidity network. Once that happens, the next bottleneck is no longer simply asset issuance or protocol design. It is trading infrastructure.

1. Trading Is Moving On-Chain, but Trading Systems Are Still Scarce

For a long time, crypto focused mainly on asset creation and protocol innovation. But the market structure has changed. Stablecoins now represent a far thicker on-chain capital base than in the industry’s experimental phase. DeFiLlama currently shows total stablecoin supply at roughly $315B–$316B. In parallel, a16z Crypto’s 2025 report estimated roughly $46T gross stablecoin volume and about $9T adjusted annualized stablecoin volume, signaling that stablecoins are not just internal quote assets anymore; they increasingly function as an on-chain dollar settlement network.

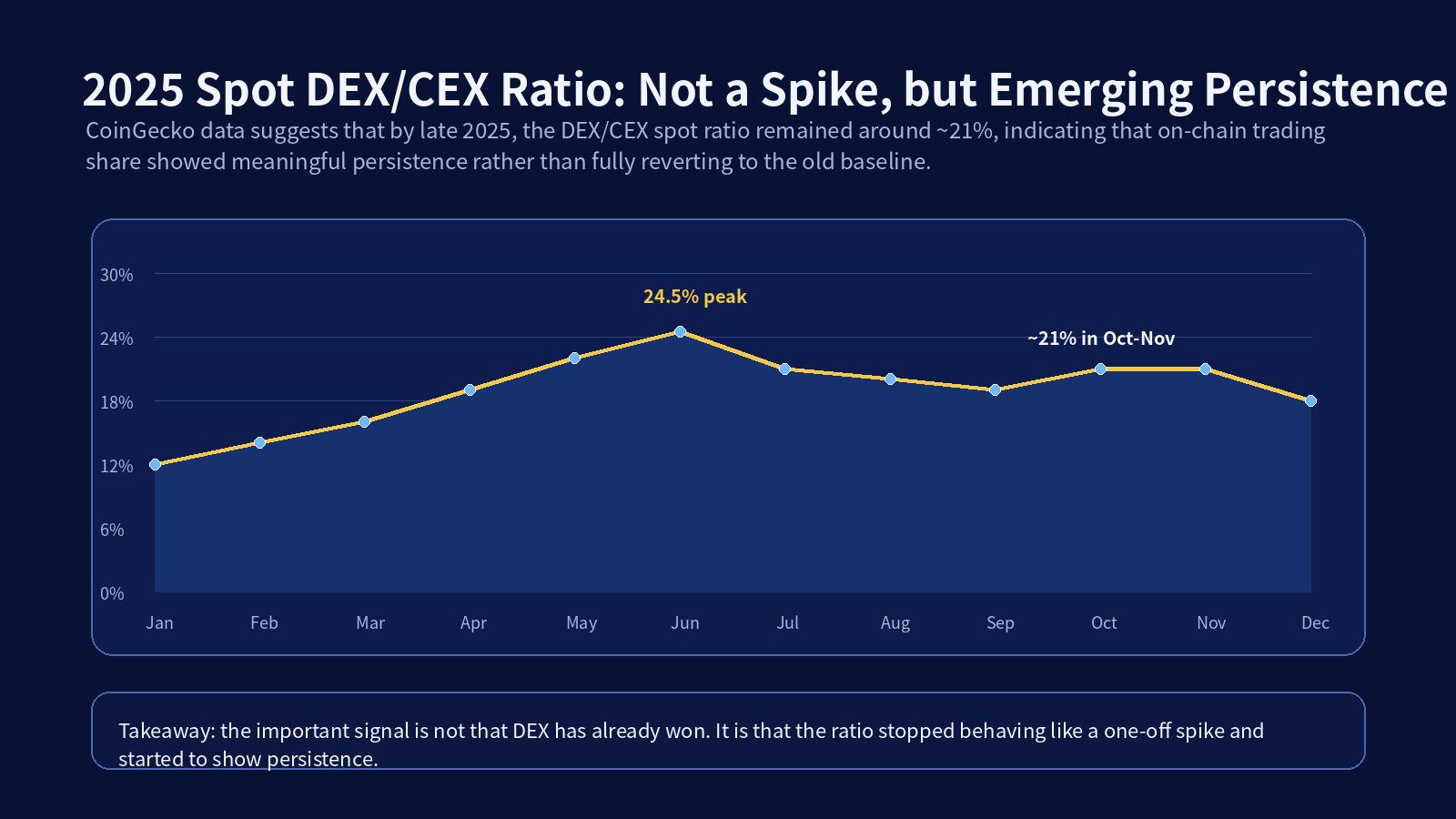

The trading side is changing as well. CoinGecko’s 2026 trading-activity report shows that the DEX share of spot trading reached 13.6% in January 2026, versus 6.9% in January 2024, and peaked at 24.5% in June 2025. CoinGecko’s 2025 DEX-to-CEX ratio report also showed that the spot ratio remained around 21% in October–November 2025, suggesting that on-chain trading share has shown meaningful persistence rather than disappearing after short-lived market bursts.

This does not mean DEXs have already replaced CEXs. It means something more important: on-chain trading is no longer marginal. It has entered a stage where infrastructure quality starts to matter more than simple existence. The scarce resource going forward is not “more tokens.” It is more complete trading systems.

2. From Bitcoin to Ethereum: Why Trading Was Always Going to Become a Core Problem

Bitcoin’s historical importance was not just that it created a new asset. It created a way to transfer value without requiring a financial intermediary as the source of truth. That was the beginning of protocol-level settlement.

Ethereum then extended the idea from transfers to programmable state changes. Assets, contracts, applications, liquidity pools, lending systems, and complex financial logic all became deployable on open infrastructure.

Stablecoins pushed this further into the real economy. Once a growing share of users and businesses hold dollars on-chain, settlement and capital movement become increasingly native to blockchains. When capital is already on-chain, trading naturally wants to happen there as well.

That is why trading infrastructure is not an optional side topic. It is the next natural step in the same historical arc:

- Bitcoin put value transfer on-chain.

- Ethereum put programmable assets and protocols on-chain.

- Stablecoins put real capital flows on-chain.

- The next stage is that trading systems themselves must be rebuilt for that environment.

3. The Market Has Already Sent the Signal: CEX Still Leads, but Migration Has Started

Reality is not “DEX has already won.” CEXs still dominate user mindshare, liquidity concentration, branding, and mainstream onboarding. But market data makes one thing clear: migration has started.

Three structural trends stand out:

- Stablecoin supply has expanded materially.

- DEX share of spot trading has risen over time.

- Users are increasingly comfortable with on-chain custody and on-chain interaction paths.

A concise way to read the market is this:

| Signal | What it means |

|---|---|

| Stablecoin supply above $315B | The on-chain capital base is no longer thin or experimental |

| DEX spot share above 10% since early 2025, with a 24.5% peak in mid-2025 | On-chain trading is no longer fringe behavior |

| Persistent DEX/CEX spot ratio around 21% in late 2025 | The market is not simply reverting back to the old baseline |

So the real question is no longer whether migration will happen at all. It is what kind of platform will be capable of absorbing it.

3.1 DEXs and CEXs Already Show Similar Head Concentration

Another useful way to read the market is not by migration alone, but by concentration structure. Both DEXs and CEXs already exhibit strong head concentration. That matters because it suggests the next generation of trading platforms does not need to “win everything” at once. The real threshold is entering the head group and staying there.

4. Why Existing CEXs and Existing DEXs Are Both Incomplete Answers

4.1 CEXs Solve the System Problem, but Concentrate Trust

CEXs offer real advantages:

- unified balances,

- clear account mental models,

- lower user-facing failure rates,

- and a “first accepted, then settled” experience.

But those advantages come from concentration. Custody, execution logic, listing power, freezing rights, internal risk controls, and order-flow visibility all sit inside the platform. Users gain convenience, but the system boundary becomes opaque.

4.2 Traditional DEXs Preserve On-Chain Verifiability, but Still Don’t Behave Like Full Trading Systems

Traditional DEXs solve a different problem: self-custody, open access, and on-chain settlement. Those are genuine strengths. But they still struggle to function like complete trading systems.

The limitations can be compressed into three structural dimensions.

A. Privacy Is Really an Execution-Quality Problem

Institutional or advanced users do not usually mean “anonymity” when they talk about privacy. They mean:

- protection of trading intent,

- resistance to linkage and pattern inference,

- and lower execution degradation as size increases.

In a fully transparent, leg-by-leg settlement environment, large or repeated trading intent becomes easier to infer. That creates impact costs, passive slippage, and shorter strategy half-lives.

B. Security Is Not Just About Smart-Contract Bugs

The deeper security problem is the end-to-end trust boundary:

- frontend integrity,

- bridge dependencies,

- external middleware,

- upgrade authority,

- price or routing dependencies,

- and incident-handling paths.

A system is not “safe enough” just because one contract is audited. It matters whether the critical path is coherent, reviewable, and governed under explicit assumptions.

C. The True UX Gap Is “Determinism + Unified Accounts”

The biggest user-experience gap is not simply gas cost or latency. It is that CEXs provide a more deterministic operating flow, while many DEXs still expose users directly to pending, failed, or reverted processes.

At the same time, the wallet-as-account model fragments funds across addresses, protocols, and interactions. That might be acceptable for low-frequency retail actions. It becomes increasingly inefficient as trading grows more active or capital organization becomes more complex.

The comparison is not moral. It is structural:

| Dimension | CEX | Traditional DEX | What the next system needs |

|---|---|---|---|

| Privacy / execution quality | Order flow is internalized | Intent is more visible on-chain | Lower intent leakage while preserving verifiability |

| Security boundary | Strong operator control, weak external visibility | On-chain settlement, but fragmented end-to-end boundary | Converged, explicit, auditable critical path |

| UX / account model | Unified balances, accepted-then-settled flow | Wallet-first, fragmented states, exposed uncertainty | Deterministic acceptance + organized account system |

5. What Is a Full-Chain Trading Platform?

“Full-chain” should not mean “put everything on-chain no matter what.” A more useful definition is this:

A full-chain trading platform is a system that tries to converge the critical paths of trading—frontend delivery, asset paths, account states, execution states, event records, audit interfaces, and governance boundaries—toward one verifiable system.

Under that definition, the next-generation platform should satisfy at least four conditions.

5.1 Trading Must Have Two Layers of Determinism

Users need more than eventual settlement. They need a clear distinction between:

- acceptance determinism: the system has explicitly received and recorded the request;

- final settlement determinism: the result has completed on-chain and can be audited or attributed.

That is not a cosmetic UI choice. It is a trading-state-machine design choice.

5.2 Accounts Must Be Organizable, Not Just Wallet Balances

Real trading is not a single swap. It is a broader capital-organization problem involving:

- netting,

- order splitting,

- internal transfers,

- limits,

- role separation,

- and exception handling.

If users are left to coordinate all of that through fragmented wallet interactions, the system remains structurally limited.

5.3 The Critical Boundary Must Converge, Not Scatter Across External Dependencies

What matters is not perfect purity. It is whether the important dependencies are:

- explicit,

- minimized,

- auditable,

- and governable.

That includes frontend delivery, asset paths, execution logic, event output, and upgrade authority.

5.4 The System Must Be Auditable, Governable, and Operable

If a trading platform is going to matter at scale, it cannot remain “just a protocol.” It must support:

- reproducible state transitions,

- structured event streams,

- reconciliation and invariant checks,

- incident containment,

- and explicit governance or upgrade boundaries.

The competition at that stage is no longer mainly about AMM curves. It is about who can build the more complete trading system.

6. Why This Route Is More Likely to Close First on ICP

This is not a claim that only ICP can build such a system. It is a narrower claim: ICP is especially well-suited to close this design loop earlier than many other environments.

First, ICP supports hosting frontend assets in canisters. That means the frontend can be brought closer to the same verifiable system boundary as the backend logic, rather than being left entirely to external web infrastructure.

Second, ICP’s chain-key token model meaningfully changes the asset-path discussion. ICP documentation states that chain-key tokens are fully backed 1:1 by native assets held by ICP smart contracts, and explicitly notes that ckBTC does not rely on an intermediary or centralized bridge. That does not remove all trust assumptions, but it materially reduces a major class of traditional wrapped-bridge risk.

Third, ICP’s canister model is well-suited for a “fast acceptance, on-chain final settlement” design pattern. At the system-design level, that makes it easier to separate user-facing acknowledgment from final settlement while still keeping the core flow on-chain.

That said, “more on-chain” does not mean “automatically trustless enough.” ICP’s own documentation makes clear that users still need to understand controller rights, upgrade powers, and whether a canister is genuinely decentralized. The right claim is not perfection. The right claim is that ICP makes it easier to express a tighter and clearer end-to-end system boundary.

7. SSS: An Attempt to Build a Trading System, Not Just Another DEX

SSS is not trying to solve one isolated feature gap in DeFi. It is trying to answer a deeper question:

Can on-chain trading preserve verifiability while also delivering a more system-like experience closer to what users expect from mature trading platforms?

That leads to four design principles:

- Push key paths on-chain as far as practical.

- Use an internal ledger to build a unified account model.

- Separate acceptance determinism from final settlement determinism.

- Treat event streams, reconciliation, and auditability as first-class system capabilities.

In the current stage, SSS is intentionally validating this architecture on stablecoin and chain-key asset paths before expanding into a broader asset universe. The goal is not maximum asset breadth first. The goal is to validate the system base first.

From that perspective, the important questions are not just about pool count or token count. They are whether the system can provide:

- a real internal ledger rather than simulated balances,

- a unified account mental model rather than pure wallet fragmentation,

- a clean distinction between “accepted by system” and “finalized on-chain,”

- reproducible trade, fee, and balance outcomes,

- and exception states that remain queryable and recoverable rather than merely surfacing as user-facing failure.

This does not mean the work is finished. The difficult work is precisely what comes next: more assets, more pools, more routes, richer market structures, stronger privacy layers, clearer quality metrics, and more mature governance. But the important point is that SSS is not starting from presentation-layer concepts. It is starting from the premise that trading should be built as a system.

8. Conclusion: Full-Chain Trading Platforms Are Not Optional

If the last phase of crypto was about putting assets and settlement on-chain, the next phase will be about rebuilding trading infrastructure for that reality.

CEXs will not disappear overnight. Traditional DEXs will not automatically fail. But the long-term direction is increasingly clear: the market will favor systems that preserve on-chain verifiability while also behaving more like complete trading platforms.

That is what a full-chain trading platform represents. It is not a marketing slogan. It is the likely next convergence point once capital, settlement, and execution increasingly live on-chain.

The real question is no longer whether such a platform is needed. The question is who will build it first as a system that can actually run. SSS aims to be one of the early builders on that path.

Suggested Sources

- Bitcoin Whitepaper: https://bitcoin.org/bitcoin.pdf

- Ethereum Docs: https://ethereum.org/developers/docs/

- DeFiLlama Stablecoins: https://defillama.com/stablecoins

- CoinGecko, The Evolution of CEX and DEX Trading Activity (2026): https://www.coingecko.com/research/publications/cex-dex-trading-activity-report-2026

- CoinGecko, The DEX to CEX Ratio (2025): https://www.coingecko.com/research/publications/dex-to-cex-ratio

- a16z Crypto, State of Crypto Report 2025: https://a16zcrypto.com/posts/article/state-of-crypto-report-2025/

- ICP Docs, Chain-key Tokens Overview: https://docs.internetcomputer.org/defi/chain-key-tokens/overview

- ICP Docs, Using an Asset Canister: https://docs.internetcomputer.org/building-apps/frontends/using-an-asset-canister

- ICP Docs, Decentralization and Security Considerations: https://docs.internetcomputer.org/building-apps/security/decentralization